A Unique Type of Coverage

Nearly every U.S. state requires that employers carry workers’ compensation insurance. Many states require it even if a business only has one employee. While workers’ compensation laws for employers vary by state, one thing is consistent: work comp is unique because it’s a “no-fault” system. This means employees don’t have to prove the employer was negligent to receive benefits. Even if the worker’s own actions led to the injury (unless it was intentional), they may still receive compensation, which is why it is so important to understand how to protect your business with proper coverage–in addition to an emphasis on workplace safety.

How Does Workers’ Comp Work For Employers: Frequently Asked Questions

With such a unique and highly regulated type of insurance, there are many commonly asked questions that arise, from how to get workers’ comp insurance to workers’ comp audit preparation. Our goal below is to help you understand the basics of workers’ compensation insurance as well as we do (or, at least close to it!)

Please see some of the most often asked questions we get about how work comp operates, along with concise answers to help you learn more about this type of insurance:

What’s considered a workplace injury?

Injuries that occur on the job or while performing job-related tasks are generally covered by work comp, and considered part of including:

- Accidents like slipping & falling, transportation accidents, and the like

- Occupational diseases from exposure to harmful chemicals, materials, or similar

- Repetitive stress injuries such as carpal tunnel syndrome

- Injuries that occur during work-related travel

What’s considered a benefit?

Benefits under work comp insurance are the financial or medical assistance provided to employees who are injured on the job. These may include:

- Medical Benefits – Coverage for necessary medical treatment for injured workers such as doctor visits, surgeries, rehabilitation, extended care, and prescription medications related to the injury.

- Wage Replacement Benefits – Compensation for lost wages due to temporary or permanent disability resulting from the injury.

- Temporary Disability Benefits – For employees unable to work for a short time due to the injury.

- Permanent Disability Benefits – If the injury results in permanent impairment or the inability to work in the same capacity.

- Death Benefits: Compensation paid to the spouse, children, or dependents of an employee who dies due to a workplace injury.

- Vocational Rehabilitation – Assistance in retraining or finding new employment if the employee cannot return to their previous job due to a permanent disability.

What’s not covered on your workers’ compensation policy?

The following are typically not covered under work comp policies and would not fall under employer responsibilities for workers’ compensation:

- Injuries occurring outside of work hours or job scope

- Self-inflicted injuries and intentional acts

- Injuries due to drug/alcohol use or criminal behavior

- Injuries from recreational activities during work breaks

- Fighting or horseplay is not considered an actual workplace activity

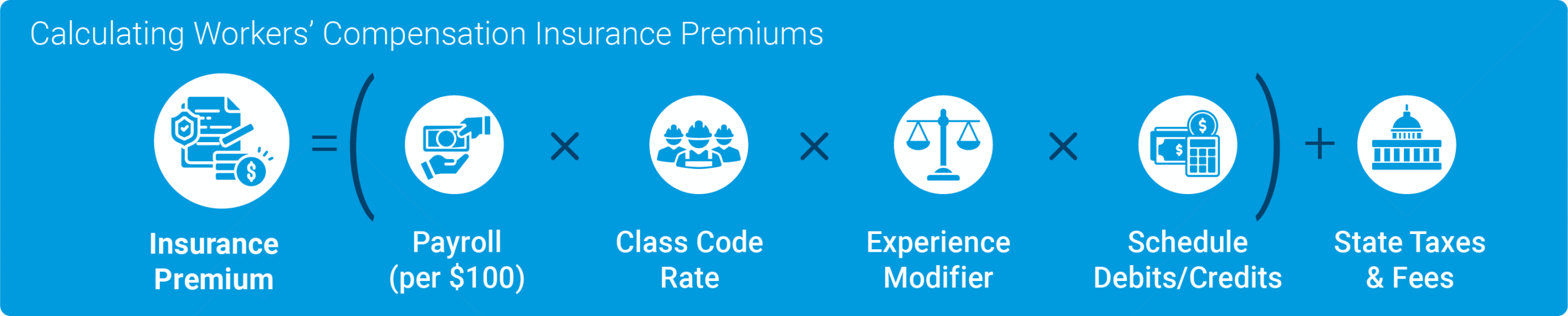

How are workers’ comp premiums calculated?

Wondering about the cost of workers’ comp insurance? Insurance companies calculate workers’ comp according to employee classification (class code) and the rate assigned to each classification. The premium rate is expressed as dollars and cents per $100 of payroll for each class code–so the number of employees and type of work both play a role. The National Council on Compensation Insurance (NCCI) determines most states’ classification rate (or the WCIRB for CA), which is then multiplied by the Ex-mod. This handy graphic may help you understand the calculation:

What should one look for when choosing a work comp carrier?

When choosing the right carrier for your business, be sure to evaluate:

- Do they have an in-house claims team (this is preferred to 3rd party)

- Value-added services like risk management consults and safety trainings

- How much they do to protect you from fraud

- Base rates

- Max schedule credit/debit filed

It’s also critical to consider reputation and financial stability. Companies that operate at an underwriting profit tend to be less reactionary with their rates.

You’ll want to ask about the carrier’s third-party ratings from companies like AM Best, as well. A high rating (like that of ICW Group) indicates that the insurance carrier can successfully pay claims and provide necessary benefits for work-related injuries or illnesses.

Check out ICW Group’s article on How to Choose a Work Comp Carrier for more on this topic.

How do you get work comp insurance?

Starting with a quote and moving all the way through renewal, take a look at the following graphic we put together to help those with questions about the lifecycle of a work comp policy:

Workers’ Comp Audit Preparation and Payroll Adjustments

Underestimating payroll at the beginning of the policy may mean a larger than necessary bill at final audit. Just be sure to keep accurate records from the start. It’s also a good idea to note that because a single employee may perform different job duties with very different risk-levels–like a shop employee who also works at customers’ locations, separating those roles out (known as wage segregation) in your record-keeping is key. For an example of a complete checklist for your final audit, see ICW Group’s Premium Audit Checklist and for more on the topic, read our article on Conducting Your Workers’ Compensation Audit with Ease.

What to do When an Employee Gets Injured at Work

Both large and small business owners need a clearly communicated injury-reporting protocol so workers know exactly what to do when someone gets hurt–no matter the size of your business operations. Serious injuries require immediate emergency care, while all other incidents should be reported promptly to the workers’ compensation carrier and directed to the designated medical provider.

How to File a Workers’ Comp Claim as an Employer

Employers should be alerted to an employee’s injury as soon as possible so that they can begin the claims process right away. If your carrier is ICW Group, you can file a claim several ways, but the fastest is to submit a claim is online. Be sure to fill out the claim form completely and accurately. See this ICW Group comprehensive step-by-step guide for more details about the claims process. Your claims adjuster will be a key partner in guiding the process, so stay in close contact to keep everything on track.

For more on how workers’ comp insurance works, see ICW Group’s article on the topic.

Have more questions? We’d love to hear from you! Please get in touch with us online or call 800.877.1111 today so we can help.